I have this Telegram group member who was trying to figure out: Given the options of money market funds such as the Fullerton Cash Fund, and fixed income funds like United SGD Fund and Pimco GIS Income Fund, how should she decide how to allocate her money at this point?

These funds are often talked about, popular but I think each of them have different attributes that make them suitable in some of your financial situations and more unsuitable in others. To some, all these funds might look similar, so how do we use them as part of our plan?

I decided to write an article to see if the article can help her better sense and decide how to use what to allocate her money.

Now.. I am purely commenting about the considerations surrounding these three funds. I am not recommending and saying these are what I would recommend.

This article ended up pretty long (despite me just wanting it to be brief. Like always), but my member should look at this article in two parts:

- Reviewing How Safe are These Funds

- How Should You Plan Around a Money Market Fund like say… The Fullerton Cash Fund, United SGD Fund and a Pimco GIS Income Fund?

I find that the first part is important because understand how safe or less safe are these funds affects your conviction in using them for planning. If you understand less, then you might not understand why I suggest something in Part 2.

But she can always jump ahead to part 2 first if that is what she is more interested in, before going back to part one to understand the why.

Okay so here it goes.

Part 1: Reviewing How Safe are These Funds

Your first encounter with these things will be when someone recommends or mentions the fund name. Or say this fund is suitable for you. Ideal for some situations.

It will tend to lead you to think that all funds are unique, not too different from the rest.

Well generally the performance of these products are different but how risky they are, and the potential performance depends on the nature of what they own.

The funds she mentions (money market funds, and funds like United SGD Fund and Pimco GIS Income Fund), are generally grouped in these ways:

- Funds that own fixed deposits (money market funds)

- Funds that own short term fixed income instruments (United SGD Fund)

- Funds that own longer term fixed income instruments (Pimco GIS Income Fund)

And then of course there are funds that own equity or a mixture of fixed income instruments and equity but that is not the topic for today.

Knowing the nature of these groups will help you decide which one (or all) are suitable for what you wish for.

But how safe are they?

Generally, these are a portfolio of securities managed by active fund managers. The managers can fxxk things up and that would mean a selected actively managed fund does poorly relative to an appropriate benchmark index.

But the real risk will be the the total risk of that basket of securities.

- Money Market Funds: The aggregate of a group of fixed deposits.

- Short Term Fixed Income Funds: The aggregate of a group of fixed income that has short duration.

- Longer Term Fixed Income Funds: The aggregate of a group of fixed income that has longer duration.

Now whether it is fixed deposits or fixed income, you have to know the nature of each of them. They are basically “I Owe Yous” or loans that you lend to issuers such as Banks, Temasek, Capitaland, Amazon for their operations. In return, they will pay you fixed coupon returns every semi-annually. At the end of the maturity period, they will pay you back the principal. Or they can call your loans back earlier and you will get the principal amount back.

These are contractual obligation. What this means is that with a single bond, there is a predictability of your final outcome (you get back your principal).

But can the issuer/bank not pay you back? Yes there is always that risk, even for a bank.

If there is this question of “How much of my bank deposits are insured if something goes wrong with the bank?” means that there is even a hint of risks there even for the safest bank. There are many small, regional banks in the US just in case you think all banks are like your HSBC big banks. Issuers like Oxley, who lend money from you always look like on the verge, skating on that thin line whether they will earn enough to pay you back.

This is what we call Credit Risks.

There were some historical scares in the past. Some of the more recent ones that are closer over here is when China Property company China Evergrande got into trouble and there were uncertainty which tranches of fixed income they might not be able to pay back.

The concern is real because some funds like the LionGlobal Enhanced Liquidity fund, which can be considered a short term fixed income fund, holds that fixed income that will mature in less than six months (if I remember well). Ultimately there wasn’t a problem there, but you can kind of see the uncertainty if you have $4 million of investable money and you plonk all $4 million into China Evergrande fixed income.

Would you be able to sleep at night?

I always felt that those of you who hold 3-4 individual bonds and they form the majority of your net wealth is quite daring to do that. Perhaps you have not flirt close to those situations.

The other risk is the Term Risk.

You should know that some fixed income mature in 4 years, some 10 years, some fifty years. Now if you want me to lend money to you for 20 years, I have to consider that money in the future is smaller due to inflation. Credit risks aside, if I am going to lend to you for 10 years, I will charge more than if you request for only 4 years.

So the returns or payments from fixed income with longer maturity will be corresponding higher.

The chart below shows the yield curve of the Singapore Government bonds as of 22 Aug 2025:

This curve shows the current market yield if a Singapore government fixed income is priced today. Fixed income would be priced with respect to this, with a premium over the rates depending on how risky they are. You can observe the 30 year yield is currently at 2.06% while the 20 year yield is lower at 1.99%. The 5 year is at 1.63%. The further is the maturity the higher a bond that is issue today will be.

But that is not always the case.

The chart below is the same yield curve of the Singapore Government bonds but two years ago in Aug 2023:

What you will notice is that the curve shape is the opposite. We call this inverted because the yield on the 1 month Government bonds is higher than the 30 year.

I know you cannot see so I list out some numbers:

- 1 month: 3.988%

- 2 year: 3.628%

- 10 year: 3.26%

If you see this, why would you lend money to people at 10 year when the 1 month rate is so high? That is why every Tom, Dick and Harry were flocking to short Singapore Government Treasury bills that has a short maturity.

So this is Term Risk.

But Kyith will I lose money if I hold a 10-year bond assuming the company can pay me back when the interest rate rises and the curve inverts again?

No you don’t lose money. The contractual obligation is there that they will pay you this amount of coupon for this long and at the end they pay that principal.

Then Kyith why is there so much worry when they say the interest rate rise? Why do they say bonds are poor in those situations?

Because if you have the intention to sell off this single bond that you bought 3 years ago, that has 7 years more to maturity today, the same issuer who issue a 7 year fixed income bond today will pay a higher interest. If the interest of the bond you hold is lower, than why would people buy it from you at your cost price? The price of your bond will have to fall, if you sell them today.

But if you hold for 7 years, and the issuer does not default, you don’t lose money.

So understand is very important if not you be confused by all these talking heads on TV or internet.

Okay how do we get the highest return?

If you want the highest return:

- Take on more term risk: Lend to people longer.

- Take on more credit risks: Lend to people who flirts on the verge of can pay or cannot pay you back.

You will earn what we call a term premium and credit premium.

But Kyith, isn’t that damn risky?

Yeah but you want high returns right?

I think you might have heard of horror local bond stories like Rickmers Maritime not being able to pay back, or Hyflux.

At some point, these issuers became really risky.

But the investors may be oblivious to that.

Greed in a way lead them to seek out return and threw caution about the potential risks, because they hope that they won’t be so unlucky.

Kyith that is a single fixed income, but will the risk be different if you hold a basket of corporate fixed income, or a basket of high yield fixed income?

The returns, and the risks you experience will be the aggregate of the basket.

And the risk of default do get diversified away. Some like the predictability of owning a single, direct bond from one issuer.

But if you ask me which is important, I will prefer the passiveness, and the technical diversification of a basket of fixed income security than 3-4.

This is my personal preference and you may disagree with me.

If I want to be so passive, I don’t want to keep worrying if some significant part of net wealth is going to implode today or tomorrow.

But if you want to be very specific with the returns, by all means. Understand what you might lose and what you might gain.

Now, what if we hold a basket of fixed income?

I wrote an article about the High Yield Bond Index, which is a basket of High Yield bonds:

The Beauty of High Yield Bond Funds – What the Data Tells Us

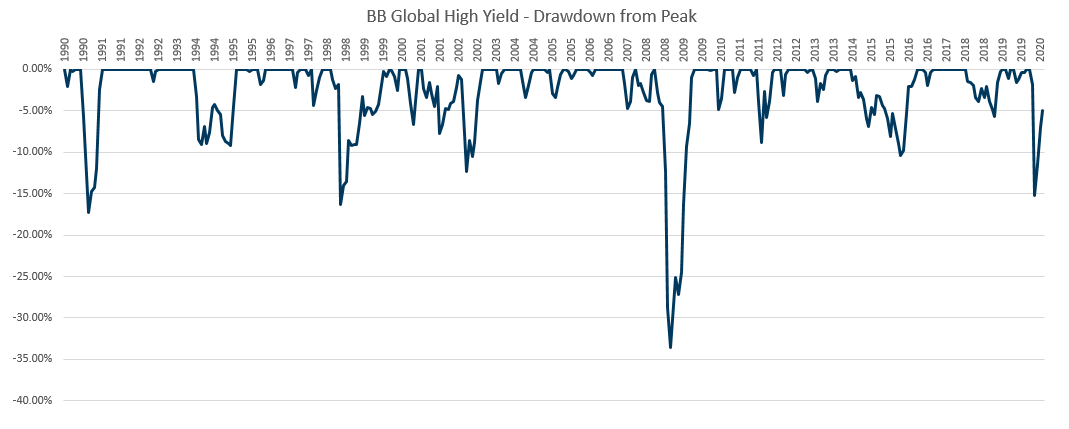

If we have 29 years of data on how a basket of 3,000 high yield bonds, we can feel the nature of the risk and return:

The chart above shows was taken from the article and it shows the degree of drawdowns for the index.

Now for my reader, your United SGD, Pimco GIS, is likely lesser risk than this. Have this frame of reference first. So what you are observing is what will happen if these fund managers, for whatever fxxk reason, decide to empty their brains and buy a lot of high yields, but in a diversified manner.

In the Great Financial Crisis (GFC), you can see a more than 30% drawdown.

There are going to be some issuers who default on their bonds.

And what you will experience is a loss in value.

While 33% of a significant part your net wealth feels painful, those high yield bonds who didn’t default and those fixed income which is reinvested subsequently will earn returns which make back the value.

I like to think going with a fund instead of direct instrument is a systematic way of preventing permanent capital impairment. Means you lose 33%, a significant part of your net wealth, and never getting it back.

You can say, aiya the returns are damn low (after 6 years), but would you rather lose that 33% and never get back?

Short Term Fixed Income Funds Should See Milder Drawdowns in Uncommon Distresses

I might have scare you by showing how distressing high yield can be but short term fixed income (like the United SGD), and for the matter intermediate fixed income like the Pimco GIS Income should see milder drawdowns even in the worse case scenario.

The fixed income drawdown in the 2022 is what I would say maybe those extreme, extreme drawdowns. This means that you can see the experiences of a short duration fund and a longer duration fund.

In one of my articles doing a deep profile of Dimensional’s two short maturity funds, I shared about how they did during those 2022 situations.

A Safe, Passive Effort Fixed Income Strategy Embedded into One Fund for Singaporeans.

The illustration below (it is a bit much) shows the profile of the two funds (Global Short Fixed, Short-term investment grade), in USD and SGD:

You don’t have to go through all of them but follow me. Generally, both funds have pretty short duration (as illustrated by Ave Dur Yrs of 0.11 years and 0.50 years).

Duration measures how sensitive the price of a fixed income security or a group of securities are, when interest rate changes. Duration is not equal to maturity but the formula to calculate it usually result in duration to be around maturity. As a rule of thumb if the market interest rate move 1%, and the duration is 1 year, the price of the fixed income in the open market would move 1%. So if your duration is 20 years… it means closer to a 20% up or down move (but its not a linear relationship, which is why i say rule of thumb. Use that as a gauge but not the final truth).

These two fixed income funds from dimensional would have an average maturity of between 0-5 years (they are active so it is not fixed), and during the time of the article, the maturity and duration is less than 6 months.

Their short duration means they are less affected by the market interest rate move from near 0% to 4-5% in less than a year in 2022.

And true enough you can see that in what I term the Great Depression in bonds, they lose a rare 6% in a year. If the magnitude is less worse, I doubt you will notice it.

What is important is that if you know this is almost the worst that could happen, you can properly financial plan for it. Firstly, you can recognize as a basket of short term fixed income, how resilient it is. You should be more convicted to be able to deploy more into it. Secondly, you could potentially over fund for your financial goals by 10%, to consider these worse case scenario and you have a strategy that tries to earn a slightly higher credit and term premium while still remaining pretty high quality and short duration.

Let Us be Very Specific to the UOB United SGD Fund

You might be a little apprehensive why I bring up another fund when you might be really interested in a United SGD Fund.

Okay, so since we know that aside from the United SGD that pays out a distribution, UOB has the same fund but does not pay out a distribution. You can review the accumulating class of United SGD Fund here.

This fund, has data going back to Jun 1998, which means we have almost 27 years of United SGD performance data.

I tabulated the NAV and the chart below shows the length and depth of the drawdowns, month by month, that United SGD went through:

There were 21 drawdowns in that 27 year history. You can see the more uncommon drawdowns are 1.5% or so. The average drawdowns you recover in 4 months. But you can see there were two deeper drawdowns.

The 2.72% drawdown happens in Aug 2011 and it took 6 months to recover.

The 3.85% drawdown happens during that Great Depression in Fixed Income starting in Sep 2021. It took 23 months or almost 2 years to recover. You can contrast this to a 20-year US Treasury fixed income fund which is still down after 4 years. The lesson specific to this is to know the average duration of the fixed income fund, and respect that in your financial planning.

I think you can make a few important conclusions here:

- We have data of how an active short term fixed income fund like United SGD perform during a 25 year period of many pivotal event.

- All the recovers happen pretty fast, within a year.

- In one of the periods where most experts say fixed income would do the worst, which is when fixed income valuations (based on yield to maturity) is the most expensive, the fund came away and recover within 2 years.

- You will save yourself a lot of heartache with fixed income if you learn about the average duration of your fixed income, and respect that in your wealth planning.

Part 2: How Should You Plan Around a Money Market Fund like say… The Fullerton Cash Fund, United SGD Fund and a Pimco GIS Income Fund?

I told you that I don’t wish to drone too much into a lot of theory but ended up spending enough time explain how safe do I think these funds are. I feel that is necessary because if I leave you with an answer “Yes it is bao jia safe”, I will be not fulfilling any fiduciary duty. If I say “it depends” and leave it as that, you would gain nothing about how to apply from this.

I would summarize the previous section as:

- Generally money market funds, fixed income, whichever duration, will give you your principal back because you are leveraging on diversification to prevent the risk of permanent loss because a small number of fixed income securities default.

- Even then, different average duration of fixed income can have different degree of drawdowns when interest rate rise at different degrees. This will impact you if you need the money earlier than it should because the funds take time to recover (and in theory they will recover unless a whole chunk of them default.) You can overcome this by understanding what is duration risks, and using the appropriate fund for certain goals.

With that in mind, we can talk more about wealth planning.

Typically, people have a few financial goals they want to fulfill:

- To have liquidity short term, but wish to enjoy higher returns.

- Have intermediate term goals like son needs to go to university in 10 years time.

- Wish to grow and preserve their wealth but not comfortable with equities.

- With to get income from an income fund or a bond fund.

The rest are different variations of this.

The first thing to keep in mind is what do you wish to MAINLY achieve with these goals. I emphasize mainly because KNN it is so common for people to want everything and in their search, they lost themselves and forget the main thing that they want to achieve.

The main objectives for the goals above should be:

- Give you the liquidity based on when you need it.

- Ensure that by the time of need, you have relatively enough money to achieve the goal.

- Make sure that the investment experience is livable, in a way you desired so that you can stay invested.

- Having a income that meets your needs (which can be rather specific such as consistency, inflation adjustment), for the tenure that you need, that is livable enough.

Notice non of them say high returns, but so many keeps chasing after that and lost themselves and forget or confuse about the primary objective.

Actually my philosophy is that aside from these primary objectives, I think people are also looking for the following two in their solutions:

- Security. There should not be permanent capital impairment.

- Passive enough.

I think some greedy people may not want number 2 so that is subjective.

Out of these four types of goals, I will touch on 1 to 3 and not touch on 4 because I think 4 is more complex. If you so wish to hear my thoughts on 4, may be you let me know.

From this point, it would be better if we identify what is the average duration, and average credit quality of the three funds we are talking about:

- Fullerton Cash: No duration risk (SGD Savings)

- United SGD: 1.8 years (BBB+)

- Pimco GIS Income: 5.4 years (A+)

Data is taken from Morningstar except for the duration of Pimco GIS Income which is taken from their website.

The returns that you will earn is likely to be the average yield to maturity of the fund (YTM for short). This gets a little blurry if you have active managers (which all three are) are likely to wholesale sell and buy new assets. We seem to observe Pimco did that for GIS Income.

Reviewing past fund returns is useless because the past returns is based on the fixed income instruments they held in the past and what the fund will hold from now, or even in the future may be vastly different. This is very different from index-tracking fixed income fund (such as the Amundi Global Aggregate Bond funds, or the AGGU of which I am vested) which has a systematic way they hold and invest the securities. This is why I prefer the index-tracking fixed income or a systematic strategy because at least I can explain the behavior of the returns better.

The current average yield to maturity of the 3 securities are:

- Fullerton Cash: 1.97% (7 day)

- United SGD: 3.2% (Aug factsheet)

- Pimco GIS Income: 6.5% (Pimco’s website)

Do note that these average yield to maturity will keep shifting, and will shift more if the manager do major overhaul.

How do we respect the average duration in our wealth planning?

In Gabriel A Lozada’s 2016 paper title Constant-Duration Bond Portfolios’ Initial (Rolling) Yield Forecasts Return Best at Twice Duration, he introduce the { 2 x Duration -1 } Rule.

Constant-Duration Bond Portfolios’ Initial (Rolling) Yield Forecasts Return Best at Twice Duration.

It means that if you respect the duration with this { 2 x Duration -1 } formula, you will likely earn the Yield-to-Maturity (or Yield-to-Worst which is more accurate because some fixed income gets called earlier and yield to worst reflects that).

So based on the current duration of the three funds (well two funds since the Fullerton Cash fund doesn’t have this problem):

- Fullerton Cash: NA

- United SGD: 2 x 1.8 years – 1 = 2.6 years.

- Pimco GIS Income: 2 x 5.4 years – 1 = 9.8 years.

So this means that if you have a time horizon for your goal that is 10 years, and you invest in the Pimco GIS Income with a yield to maturity of 6.5% (if they don’t change it too much), you will earn 6.5% p.a. for 10 years. So for United SGD is if you hold for 2.6 years you should earn 3.2% p.a.

What if you hold longer or shorter than that?

Then your results would vary.

Corey Hoffstein of Newfound Research put this chart which shows the relationship between the yield-to-worst of the Bloomberg US Aggregate Bond index and if you respect this { 2 x Duration – 1} rule:

You can see the relationship there but it is not perfect.

But this is a clearer relationship than anything you can get with equity, which makes fixed income so unique (and boring, which sometimes is good).

It allows you to have some predictability for your planning especially because your goals is within these 10 years.

But Kyith what if the fund managers overhaul the portfolios?

If they do that then of course the dynamics will change. The yield to maturity (or worst) will change and therefore the returns. But you got to recognize that yield to maturity and this rule gives some predictability but to a certain degree.

In practice, most funds have a certain mandate to keep within a certain duration.

For example, in the two Dimensional funds in the Great Bond Depression segment, they have a mandate to hold fixed income with maturity between 0 to 5 years. The fund managers at Dimensional have to respect that.

And in a way United SGD and Pimco GIS might have something similar.

But there are also funds which are pretty unconstrained, which means they can do just about anything. Not sure if Pimco GIS is something like that.

At the end of the day, if you have a specific financial goal, some potential investment tools might give you more uncertainty that you can lived with. It makes sense to use the more appropriate tools (known duration, based on their implementation so that you can target returns for the time horizon better).

Planning for Your Child’s Education 10 Years Later

We will start with the Goal Type number 2 which is a goal with a pretty fixed time horizon because this has more complexity that is most related to what we want to talk about.

I will use my nephew as an Avatar to illustrate. My nephew is almost turning 9 years old in 3 days time. As a male most likely we will need to get ready an amount of money for his tertiary education when he turns around 21 years old.

If we are planning, we can plan to have the money ready one year from 21 years old. So that means there is almost 11 years till the start of 20 years old, or 12 years till the end of 20 years old.

An annual tuition fee on average is $8k to $9.5k a year if we don’t include law, dentistry and medicine. Let me use $10k to make it easy and that will be $40k today for a 4-year degree. (Don’t ask me about the what ifs of something more expensive because that is not the context of discussion.).

If we estimate an inflation rate of 3% p.a. for 11 years, that will bring us to $55k. If 4% p.a. its $61k. Let’s try to accumulate $60k, which gives a nice buffer for a slightly higher inflation rate.

Given the time horizon of 11 years, we can actually use the Fullerton Cash fund, United SGD or the Pimco GIS Income fund. This is because the fund with the longest duration is the GIS Income fund and based on the {2 x Duration – 1} rule, all of them are shorter than the time horizon, which means we can hit the yield to maturity. However, the Fullerton Cash and United SGD have shorter duration which means although you could earn that yield, the fund needs to kind of reinvest two more times and the yield to maturity will depend on the interest rate and credit spread 2, 4, 6, 8, 10 years later.

That will be pretty hard to plan. You can use the current yield to maturity as a planning return but you got to recognize that likely the returns will be different.

If we are optimizing the potential return, while being sensible in our planning, using the Pimco GIS Income fund will be the most appropriate. If the current yield to maturity is 6.5%, and our time horizon is 11 years, we will need to put in $30k today.

You can use a time value of money calculator such as the one here to help you with here.

Now let us discuss some potential questions around this.

Kyith, the time horizon exceeds that rule by about a year, would that be okay? Wouldn’t my eventual return be less precise?

Firstly, remember that {2 x duration – 1} rule is at best an estimation based on empirical research around a problem. Even if they did a lot of work, your returns is not going to be precise.

It is more accurate but it is not going to be precise.

If your time horizon exceeds this rule by 1-3 years, your eventual return is going to be less accurate.

But you should never forget that your eventual returns are going to be in a range and its just the range with fixed income is much tighter than equities, and it gives more predictability. But it is not going to be that precise that you end up like bank interest (then again bank interest is only precise over a very very short period!)

Kyith, what other things can I do to make my Kid’s education more certain?

By using fixed income, and doing prudent planning, we should recognize that we are doing our best to have some conservative accuracy.

If you want to make your plans more certain, fund the amount set aside for the kid’s education more, but keep to the same portfolio.

So instead of funding $30k, you could fund $40k or $50k.

If you don’t have the money upfront, you can fund $30k, then top up more if you happen to have more bonus to make the plans more conservative.

This would be very different from some of the advise my colleagues give at work. Which is “you don’t need to take risk, you actually have enough money, just put all in cash.”

I think everyone in a way are trying to optimize their allocations by balancing time, not missing out on returns, but also fulfilling your goals. Our outcome depends on luck.

By putting all in cash, yes you achieve certainty, but it is also contingent that inflation is zhun zhun 3-4% p.a. I think people with some greed would not sleep well if they just dedicate large chunks of money to cash. In my mind, the most optimum way is to take enough risk but not over do things so that you can potentially benefit if your situation is not too bad.

Here is the outcome:

- If you end up with median to very optimistic return: Your child has money for university and you have excess money that can potentially be reallocated.

- If you end up with very pessimistic return: Your child has money for university.

And we should not forget the goal of what we are accumulating for.

Remember that You Need Not Make All Plans So Conservative

What I am sharing is if you have a goal that is particularly inflexible, that you die die need $60k at the end of 11 years, how to make the plan more certain.

But you might not need to do that.

There are goals that you let some fate to decide, after some prudent planning.

So you can mix and match. If you overfund your goal, you could technically use United SGD if you wish to. Don’t have to measure so accurately.

And while I am here, this works for other goals that is equivalent such as setting money aside for the downpayment for a condo or what.

All the rules apply.

The important question to ask is how inflexible or non-negotiable is that sum of money.

Managing Your Liquidity

Singaporeans have too much money and I think many would fall into this camp.

Liquidity means your time horizon is very short. Like for some maybe the next day. But for many that have $400,000 (because they are rather conservative, have this investment warchest idea, or genuinely feel more safer to have more cash), you can genuinely break into different liquidity pools.

But before that, I think it makes more sense to mentally ask yourself if part of this money is for liquidity, and part of this money is because you don’t know what to do with the money, or you are preserving your wealth and don’t dare to take risks with it.

I am big on the idea if you mentally frame what the money serves/buys you, you can have an easier time finding the solution.

I feel commonly the cash people have is part liquidity, part investment warchest or for other goals.

And in this part I am mainly talking about the former, and we will try to tackle the latter in the next section.

Even in liquidity it is likely you will have money that you need:

- Tomorrow

- Possible within 1 week

- Possible 1 month

- 3 months.

I would always wonder if I have an emergency and all my money is in 6-month Singapore Treasury bills what will happen.

This is quite a good exercise to think through. Which is why much of the 6-month Treasury bills are actually capital preservation for risk averse people. I don’t think its even investment warchest because opportunities might not wait 6-months.

- Funds required immediately: A higher yield savings account like DBS Multiplier, UOB One or OCBC 360

- Funds with 1 week liquidity: Unit trusts from most unit trust distributors. If you sell a fund, you should typically get them in T+3 business days but some might take slightly longer.

- Funds with 1 month liquidity: Singapore savings bonds

It will all depend on your own philosophy behind liquidity needs. Very difficult for me to say.

If we look at the three funds, the Fullerton Cash fund and United SGD fund are more ideal.

Technically if you expect $50,000, the Fullerton Cash fund should give you $50,000 because they are deposits. Although the LionGlobal Money Market fund did went negative during GFC. I have shown the drawdown that could take place and how long they can be for the United SGD fund.

For those who are more greedy for more passive returns, and would like to go further out and take on more credit and term risk (but not too much), the United SGD fund is more ideal.

Everyone needs to manage their expectations in that, if they want higher returns, they might have to accept some volatility. If you kind of understand that a short term fixed income fund is quite the sweet spot in my opinion.

For those with more resources, you could maintain more liquidity than what you have in mind.

Here is the outcome:

- If your short term fixed income fund is negative exactly at the time you need the money: You have adequate money that you have in mind, because the volatility reduce the amount but you still have enough.

- If your short term fixed income fund is positive exactly at the time you need the money: You have adequate money that you have in mind, with the rest just growing normally.

Kyith, if I am a Retiree and I withdrew a Year’s Worth of Income to be Spent, Should I put them in a Fullerton Cash Fund or United SGD Fund?

Ideally the safer option is to just put all in Fullerton Cash Fund. If you put in United SGD Fund, there will be some years the value temporary takes some hit, to the degree of 0.5% – 1.5% like that.

I leave it to you to manage.

Preserving Your Wealth for More Risk Averse People

Preserving wealth in my mind is basically you have too much money and don’t know what to do with it, but you want it to grow decently. Yet there might be a possibility you would need to reallocate the money. You just don’t know when.

If you are looking at this pool of money for income, then this is not wealth preservation. That is an income goal, which I would not go into for this article. If you need this money to make a down payment to build a new home, that is also not this goal, check out the “Planning for Your Child’s Education 10 Years Later”.

If we don’t have a time horizon, but there is potential need to re-allocate the money earlier it will translate to a few attributes we need for our portfolio solutions:

- The portfolio should take care and not suffer from severe drawdowns (because potentially you might need to re-allocate anytime)

- It should have elements that tries its best to keep up with inflation (because you won’t know how inflation is in the future.)

Ideally, if you have goal-less money a more balance portfolio with half diversified equity and half fixed income makes more sense. It will have elements that fit this. Some of the worse 60/40 drawdowns is about 20-25%.

And if you know how bad some of the worse drawdowns are, you can have a good mental picture in pessimistic cases you have how much to work with.

However if you are risk averse, and you are left with fixed income, I think the Pimco GIS Income is more ideal because you are taking on some credit risk and some term risk but not too much.

In that Bond Depression of 2022, Pimco GIS lost 8%, which is pretty commendable if you compare against the benchmark index, Bloomberg Global Aggregate Bond (SGD Hedged) which lost 13%.

When you are balancing trying to get returns and volatility, you got to accept at times there will be losses.

We cannot get a straight line 5%, 5%, 5%, 5%, 5% return and if you see something like that, it will lean closer to a fraud then a good opportunity.

Wrapping Up

I hope this article gives my reader some good ideas how to differentiate between the Fullerton Cash, United SGD and Pimco GIS. She should always think from the perspective of how they will help her reach her financial goals.

You would realize I didn’t talk a lot of returns because if you are more opportunistic, more active, and looking for hints what to do with your money given the interest rate situation, finding Kyith is probably not the right person.

And I am not sure if it is worth it because most people will either get some calls right or some calls wrong.

The three funds mention have different maturity and duration profiles. Transitions from normal to inverted, you should hold Fullerton Cash Fund. If the is upward sloping, and slop upwards more, you should go with Pimco GIS Income fund.

If the whole curve shift up, you should not be in Pimco GIS Income fund but in Fullerton Cash Fund. If the whole curve shift down, you should be in Pimco GIS Income fund.

And I am just talking about one yield curve (the Singapore one), if your funds own fixed income in different countries, they would move and slope differently.

I think you find someone that gives you better ideas lah.

I prefer to go watch Kaiju No 8, Gachiakuta, Dan Da Dan then think about this.

But since I have tabulated 27 years of United SGD (Acc) fund returns, here is the rolling annualized return:

Each point on this chart is a 3-year annualized return. The compounded average return over this time frame is est 2.91% p.a. (UOB list it at 2.97% p.a. since inception so my figures not too far).

But as you can see, if you hold it for 3 years… your return really depends. You will have to accept that variability in returns is a fact of life. But I hope that this article provide some practical ways to craft some sensibility into your plan.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.