At the start of the year, I would usually report how much I spent in the past year. In this post, I will share my spending in 2024.

I learned from somewhere that we would usually allocate our income with this framing:

- Spending for today – These are our current expenses.

- Spending in the past – These are the repayments on the debts we owe.

- Spending in the future – These will be our savings and investments. They are meant to fulfil a life goal in the future, which will require some money.

You can decide how much to spend for today, the past and the future.

There is a tradeoff to saving up money to spend in the future, and we should all recognize that. Unfortunately, some fail to recognize the tradeoff, and they struggle with living life with money.

Reviewing our spending is a way for us to be more conscious about our spending.

My Past Annual Income Spending Breakdown

Updating my spending has become a customary update on an annual basis. Not everyone may be interested. However, if you have that little voice inside wondering why the spending is this way, you might want to take a look at what I blabber about in the last few years:

- 2014: $23,798/yr – A review of my past year’s expenses

- 2015: $22,150/yr – How our family’s $22,150 annual expenses mean for our financial security and financial independence

- 2016: $26,238/yr – My Annual Expense Report – $26,238/yr and its link to Financial Security and Independence

- 2017: $21,723/yr – Annual Expense Report 2017 – $21,723

- 2018: $19,655/yr – Annual Expenses and Financial Security Musings

- 2019: $23,186/yr – Spending Report for the Year

- 2020: $22,464/yr – How I spent $22,464 in 2020

- 2021: $27,680/yr – Annual Expenses Report 2021

- 2022: $39,187/yr – Annual Spending in 2022

- 2023: $29,554/yr – Annual Spending in 2023 – Reflection of Spending Consciousness

In the first 3.5 years, the expenses comprised three adults’ spending. The expenses were spent on two adults for the next 4.5 years. The current spend (not included in the list above) is the spending of one person (me).

How I Classify My Spending

There have been a few changes in how I classify my spending.

I think if you are on this path of figuring out how to track, budget and reflect upon your spending, you are going to look at things differently. The more you learn, the more you will calibrate how you look at your spending in a way that fits your needs the most.

I revamped my spending last year after my dad passed away in 2023. The current system fits more for a person monitoring their path to Financial Independence.

I have written extensively about how I think about my personal money situation in My Personal Notes section.

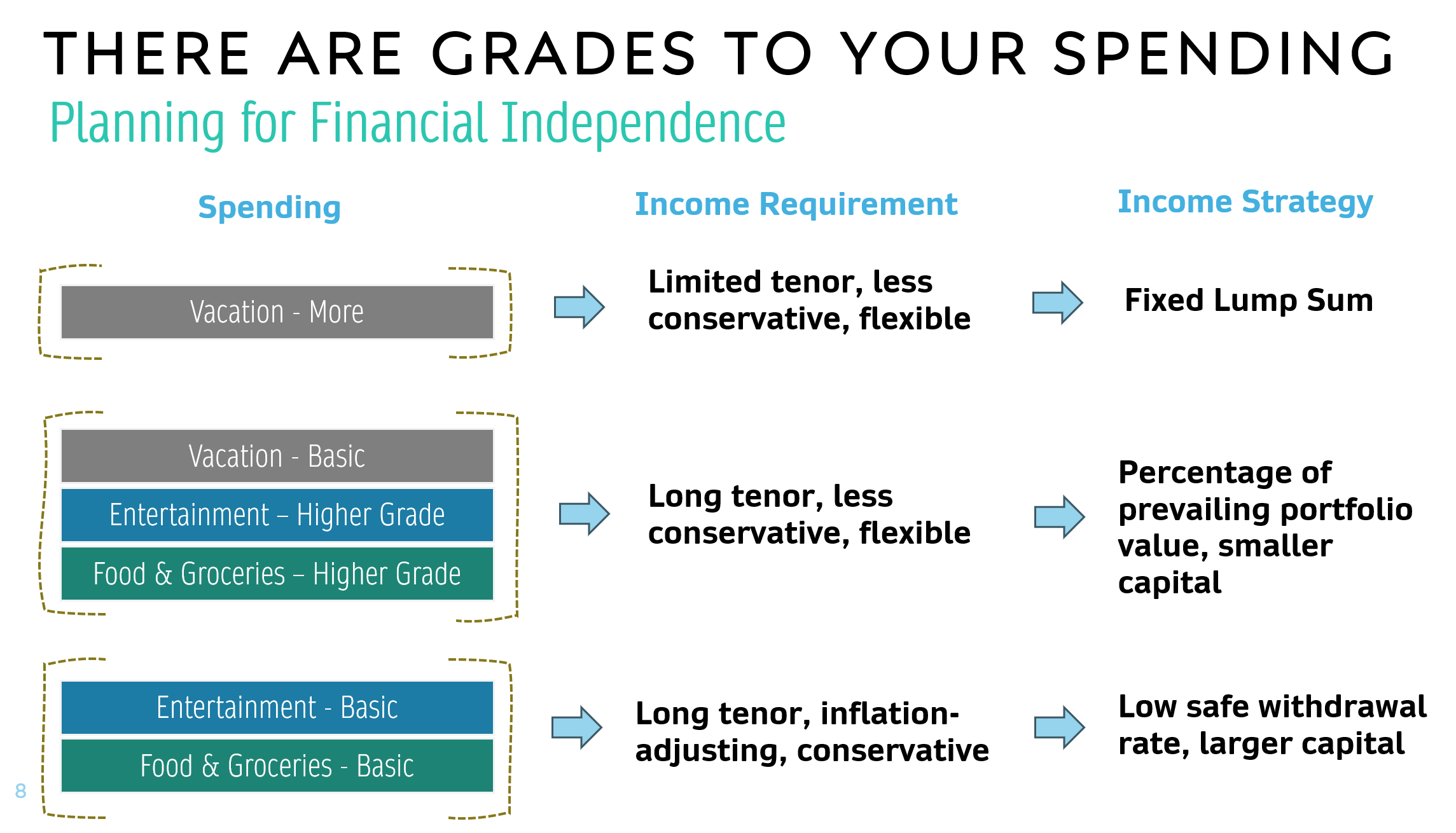

Generally, they are grouped so that I can review specifically the following areas:

- My most essential spending (You can read about them in each article). Most inflexible and needs to be most conservative.

- My basic spending. Often inflexible but the timing of spending can be flexible. Mostly conservative.

- Spending if I work.

- Spending that would come from portfolio sources.

- Flexible spending. Can be adjusted, scale up or down depending on market conditions.

The difference between each spending group is based on critical planning characteristics:

- How flexible or inflexible is the income/spending needs.

- Does the spending requires inflation-adjustment.

- Whether the spending is gong to last forever or it ends after certain years.

These critical characteristics affect your income strategy in the following way:

The above is more like an example, not how I want to plan out.

The more inflexible, inflation-adjusting or long the spending needs to be, the more conservative your income strategy needs to be.

Thus, how you look at your spending matters.

Ok let us take a look at 2024’s annual spending.

2024 Spending – $41,923 in the Year

Here is how my spending looks with the new breakdown:

My total spending for 2024 comes up to be $41,923. This is higher than my spending in the past two years.

You can see the monthly spending as well as the total and average at the bottom.

I really like the rainbow header for the table Ha Ha Ha! This is probably the highest annual spending I ever had but yet in a way, I didn’t hit what I sought to achieve at the start of the year.

I will spend the next few sections to explain each group in detail.

Essential Inflexible Spend – $4,459 in the Year

The essential inflation spend is a category that I have my eye on the most. This is the inflexible spending that is most essential to life and if this goes up based on inflation, then I have to spend this in a way.

I reflected upon this category and came up with the following budget for income planning:

Updated 1 Dec 24. Click to view a larger table.

The spending is to be provided by the Daedalus portfolio that I frequently wrote about, with the most recent one here. You can read about why I list these items and the corresponding amount in this post.

Reviewing the spending in this category is to see if this template still make sense.

My spending here in 2024 is about $1000 higher than in 2023. But this is still below the $9,800 provision in this template. My essential food and groceries and transport is not too different from 2023.

The bigger difference is the Utilities, Conservancy and Essential Replacements which is $2,239 versus $872 last year.

For clarity the common items that goes into here are:

- Property Tax – $172 annually this year

- Broadband – $38 monthly this year

- Personal Mobile Subscription – $15 monthly this year

- Town Council Charges – $78 monthly this year (without subsidy)

- Utilities (Water, Gas, Electricity) – $60 monthly average

- Laptop Replacement

- Mobile Phone Replacement

- Refrigerator Replacement

- Toiletries

I probably provision a budget of $2,920 annually for this and so spending $2,239 is still within the limit. This year I replace my mobile phone after 2 years and so I spend about $365, which is something I did not spend last year. Among the spending, I actually paid last year and this year’s property tax so that bumped up the annual property tax by quite a bit.

I think this review also made me realize I missed out on a very fundamental item in my essential inflexible spending budget: Property tax!

I will have to spend on this yearly, and regardless of how much my flat is valued at, I have to pay this. So this is something that I will be revising that budget shortly after this post.

My food spending of a total of $1,100 is low compare to about $4,320 because of a few reasons:

- CDC Voucher subsidizing grocery and food spend.

- Meal prepping. You can read about my meal prep here.

- I would usually eat 2 meals a day.

There are those who say the cost and time is not worth it but with the basic food cost approaching $5-6 per meal, food prepping becomes more worth it. Still I do set my budget as $6 per meal for 2 meals a day. With meal prep, I do average $6 in food cost a day. But as you can see the food cost is even lower.

As a worker, the transport cost averages $100 a month but if I am not working, I do think this will go down dramatically.

Another thing I notice that is interesting is my utilities. I will always have this feeling I did not record down my utilities payment in my budgeting app ActualBudget but I cannot find the transaction.

Turns out my utilities look very weird:

What you see is that there is a lot of negative amount. That means I don’t have to pay for that month. Turns out, I completely forgot about the GST U-Save Voucher. What surprised me was that the amount not used is brought over.

So I ended paying like $60 for gas, water and electricity in the whole of 2024.

Lastly, I have 2.5 months of Town Council fee rebate in the year.

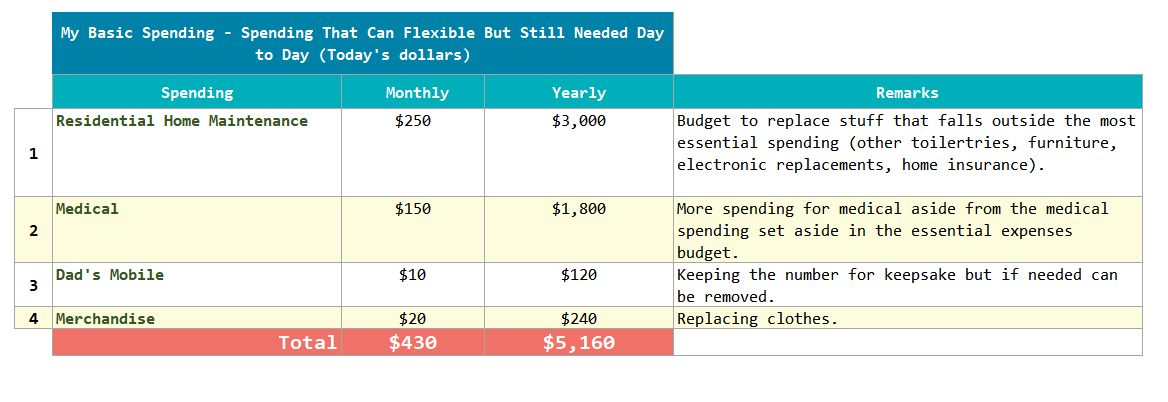

Basic Inflexible Spend – $2,266 for the Year

The Essential Inflexible Spend are the spending that allows a person to run for a long time at the minimum.

However, the reality is that you would have to provide for more in the house. Things break down in the home and you want to improve things over time. You also want to provide for more medical needs. You will have to spend on basic inflexible spend but if market conditions are not so good, you can shift when you spend it. But you would ultimately have to spend and cannot cut down much.

I wrote about provisioning $5,160 a year for things like this:

You can read more about this in this post here. This spending will come from Daedalus income portfolio as well.

I spent $2,266 in 2024 and this is higher than the $1,482 spend in 2023. This is still lower than the $5,160 provision in the year.

Whatever is not spent here (about $3,000 here) is accumulated annually. This is especially so for the excess $1000 in residential home maintenance which will eventually be needed to replace something pretty necessary such as washing machine, painting, 10-15-yearly renovations.

You might also notice that the spending is pretty lumpy and if you are less seasoned with budgeting, you might struggle to make sense of it.

There is a whole bunch of things that go into here notably:

- Kid DuoRest Ergonomic chair – $43

- 5 x Stainless Steel container for better meal prep

- Electronic Kitchen measuring scale

- Mayer Glass Airfryer because there is a Singles day discount and it is always good to have another airfryter – $69

- Roborock Qrevo S Robot Vaccum (that has not come yet after two months!) – $361

- Rattan Chair – $23

- High pressure shower head – $9

- Yeelight bulbs

- Many storage containers

Flexible Spend – $25,734 in the Year

Flexible spend is what you would call the Discretionary spending. The kind of spending that makes life meaningful. This is also the spending that you think you can be flexible about.

Why does this matter in your income planning?

If you are really flexible with this, then if the portfolio is not doing well, then you can cut your spending. You have to deeply reflect if you can cut this.

Aside from income tax, flexible spending is where I spend 60% of my annual spend.

Last year, I spend $16,569 here so this is more.

I am still contributing to nursing home expenses for my grandma although I was told there is less need to this year. Still, I think we should eventually plan for a day where we won’t get so much subsidy so I continue to contribute. Why are there some $0 gaps there? Because I do forget to transfer sometimes.

Premium meals are the discretionary meals I spend out celebrating events, treating friends and family. If I am doing well, there will be more and if not, this will be more controlled. This amount is not too different from last year. I don’t control my premium meals and this is very volatile but they somehow don’t change much.

The fun and hobby spending is lump under Entertainment and Hobbies. This is where my nonsense spending is and this went up like 100% this year. Providend Gifts are the spending that happen accidentally or intentionally because of where I work. This year’s spending is just slightly lower than last year.

Sometimes I wonder how much of Providend Gifts and Hobbies are made up of second hand monitors. I probably bought like 14 monitors and monitor arm this year. Lets count:

- HP E272Q – $45

- Dell U2413 – $15

- Dell P2715QT – $73

- Samsung M7 32 inch 4K monitor – $135

- Dell U2714 HMT 2K – $65

- Dell 2715 2k Monitor – $70

- Dell 3415W – $50

- Dell P3418HW – $73

- ErgoEdge arm – $20

- Dell P2715Q 4K – $100

- Asus 28 inch 4k – $140

- Dual monitor arm – $15

- North Bayou Dual Arm – $17

- Dell UP3017 30 inch – $52

- Samsung 28 inch 4K – $80

- Dual monitor arm – $18

- Monitor arm x 2 – $10

- Dual monitor stand – $10

- Ulti monitor arm – $17

- Acer 27 Inch 2k gaming monitor – $90

- Monitor arm x 2 – $25

- Monitor arm x 2 – $16

- Dell 24 inch – $10

- Dell U2715H – $50

- Dell 24 inch – $20

I have also bought a few computers:

- GMKTec G5 N97

- Lenovo X270

- Dell Optiplex 7040

I also decided to gift more to charity this year.

The only holiday money comes from the cycling trip in Taiwan early in the year.

The Rest of the Spending

The rest of the spending includes:

- Income Tax under Work

- Insurance Premiums under Funded by Net Wealth

My income tax is a function of work and blog income. If there are inflows, this is a necessary outflow. Don’t have to think about it so much except to have enough liquidity to pay for it.

I have set aside capital to pay for future insurance premiums so that won’t come from the salary. You can read about it at Cutting My F.I. Capital Needs for Insurance Premiums from $131,366 to $58,132 by Prepaying for It.

End of the Year Spending Reflection

There ain’t a lot to learn from study how I eat, move about and spend on the things that keep the household going after doing this for the past decade. Yet, I did easily missed out certain things in my spending that I ought to know such as property tax, and certain subsidy.

While tracking your spending is important, review and reflection is where the value is.

How you frame or group your spending is quite important because it makes it easier to see what you want.

I shared with a Telegram group manner some grouping adjustments he can make to his spending. I explain to him that grouping it this way allows him to zero in based on his different responsibilities and area of concern:

The grouping that may be more critical for a family man can be different. This group helps for someone thinking about financial independence because it better allow him to peel away parents, family if he wishes to see what he can control more (Personal). It also allows him to easily deduct some spending that will go away over time (parents and children) and see how this affects the FI capital he wish to build up to.

While there is no right way to budget and track spending, I think there is a degree of sophistication that you can consider and I shared some of them here today.

Our budget should reflect our values and how we wish to live our life. The budget might reflect fear, conservatism or abundance.

How I Track and Budget My Spending

I use a free and opensource self-hosted YNAB-style Envelope budgeting system call Actual Budget.

You can read up about ActualBudget here.

A YNAB-style envelope system allows us to see how much money that is accumulated in an envelope over time. This is something a lot of other system struggle to design.

ActualBudget’s reporting have improved by leaps and bound.

I was able to come up with this article with the help of the reports and the transaction filtering.

I created a series of YouTube video of ActualBudget including how to install, setup your budgeting system.

You can view the playlist here.

But I also notice the nice thing about it being free is that there are more and more YouTube videos on Actual Budget. This is great because it creates a bit network effect.

Usually, I don’t publish my monthly spending here but if you are interested I do publish them on my Instagram. If you are interested you can check it out.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.