I have this Telegram group member Rootie who was asking us about how we look at a medical sinking fund. If you wish to join my Singapore Financial Independence Telegram, you can join here.

Here is both his question:

Would like to check if this sinking fund invest port/mechanism makes sense?

The intended drawdown is up to 30% of the portfolio for sudden medical expenses and let the investment returns recover it over 5 years, its inflation adjusted and because the drawdown is up to 30% and needs to be stable, this 30% allocation will be in bonds and the rest in global equities.

and

Want to share what I’m planning to do with the medical sinking fund.

I have tabulated 4-5 years annual medical expenses based on my employer medical claims and did some a 1.5 times estimation from there.

I asked an LLM to run an estimation on the asset allocation and derived a 10% drawdown with 5 year replenishment. Will accumulate the funds and stop at 100k (around 20% bonds 80% equities).

I’m doing this as I don’t have very good insurance coverage so have to make do with this plan.

I can empathize with Rootie.

I always find some of us are more motivated about certain niche areas of planning because of how it touched our lives.

This is not the first time I written about a sinking fund.

A sinking fund is basically a pool of money today, that you designate to a specific goal/purpose so that you can have a peace of mind that you have set aside enough money when you need it. You separate this from your other goals because you can easily recall how much you have for the need anytime you zoom in to it.

Off my head, I can think of this for different purpose:

- Your child education is a common one.

- Medical needs is another.

- Major home maintenance needs like 10-15 years one time one is another.

Usually, how you size the sinking fund really depends on how unique your spending needs are.

I wrote a couple of pieces about how I plan my medical sinking fund in my Personal Notes section:

- Sinking fund for majority insurance premiums for the rest of my life.

- Sinking fund for future health insurance premiums.

- Sinking fund for my critical illness needs. And for my friend.

After a while, you will realize that my sinking fund concept is pretty standard. There are some considerations which I will go into later.

I have come up with a Google Spreadsheet to help readers figure out: How much do you need for your ______ sinking fund today?

I will introduce the spreadsheet to you and then we will briefly go through Rootie’s considerations.

Get My Crisis Sinking Fund Google Spreadsheet

You can make a copy of my Google spreadsheet here >>

How the Crisis Sinking Fund Works

Here is a snapshot of how my spreadsheet looks like:

The cells that you are suppose to fill in things are in yellow, and if it is not in yellow, it will be computed for you. I have set up warnings if you try to edit other cells. There are about 100 rows, and should span longer than 100 years old.

I will go through what to fill in based on the numbering:

- This is the inflation rate of the amount you need in a crisis. Usually you can use 2-4% p.a.. The higher this is the more stressful it will be on your sinking fund.

- This is the return of your sinking fund. This depends on your asset allocation into what kind of risk assets. You will notice there is a median and conservative return. The reality is that the return that you will experience in the future is a single draw out of many many possibility. But what you would like to appreciate is if your experience is normal and if your experience ends up damn shit. So conservative is for you to put a lower, more pessimistic figure so that you can see how that looks like.

- You can put the current year, or the year of planning here.

- You can put the age of your next birthday. For example Kyith’s birthday is only in November but we assume that if he turns 46 after November, we input 46 here.

- Number 5 is the starting value of the Crisis Sinking Fund. What do you put here? We will go through later.

- You will notice a column of cells for you to put in the value of your crisis. This allows you the free play to put in how much you think is the kind of crisis you wish to simulate. The spreadsheet will calculate the future value of the crisis based on the inflation rate for you.

There are two cells above Sinking fund current value to aid you in seeing when your sinking fund goes negative or it nevers.

This spreadsheet should be flexible enough to help you size up your sinking fund.

My Sinking Fund Framework

My idea for figuring out how much to set aside today (which is that number 5 in the previous section) is very standard one.

- You put in what you want to plan for [inflation, portfolio returns, how the crisis spending would look like over the rest of your lives]

- Then you keep increasing the value in your starting sinking fund value until you feel okay with it.

That’s it.

This make sense… if your other inputs make sense.

- If your portfolio returns are unrealistic, too optimistic relative today, your sinking fund fails.

- If your estimation of the amount of needs, the frequency of needs is unrealistic, your sinking fund fails.

The reality is… if you ask your sinking fund to do a lot of magic, you will need a lot of money.

We all have to balance some realism and imagination in this kind of planning.

I think the key also is what is your conclusion

- The most important thing is going through this exercise to know if you have set aside enough,

- and how thin or wide of a safety margins you have in your plan.

- firm up what is your asset allocation.

- decide among your assets, do you have enough for this, and if not this is the amount to save up.

What is slightly more unique about my framework is the two level of returns.

If you are planning for these stuff, I don’t think you want to be too risk seeking here. The two level of returns allow you to appreciate if markets are normal and if it is too pessimistic.

Every bugger will ask me: “Kyith do you think it is a good idea to put in 100% equities? Can a Pimco Income Fund be better?”

And the truth is I don’t know. If you are lucky and the return nice nice, then it won’t be a problem right?

But what many struggle with is not sure what is the return experience like in the future. I also not sure what.

Planning is not expecting.

Planning is trying to appreciate if things are poorer than your expectation, would your situation collapse?

I think this is what gets your anxiety up.

Now lets go through some of the ideas.

Can a 30% Drawdown Recover in 5 Years?

Rootie plans for the size of a crisis to be 30% of how much he funds it:

And we can just give it a try and you can appreciate if it works.

In this case on a portfolio that returns 6% p.a. on median but 3.5% p.a. when it is pessimistic, you can see the value before the spend, and 5 years later.

Depending on how you count 5 years, with a 6% p.a. median return it would recover but if returns are pessimistic it would not.

Does that answer his question?

I don’t know what he is trying to find out like what works or not. If I was planning this, and I expect such a degree of drop every 5 years, then I will ONLY look at the conservative returns column.

Typically, returns drop by 50% when pessimistic. If your portfolio is more volatile, then it gets even worse.

This is why I would prefer a balance portfolio than a full 100% equity. You have to consider the drawdowns or sequence of returns.

I tried to see if inflation make it more challenging in the later years:

There are some nuances there but objectively you can see the conservative returns may take more than 5 years to make up for it but you also have to consider:

- After 20-23 years, the sinking fund returns would more likely lean to the median (but not the median) and your experience may be better.

- You also have to consider how much more you wish to provision for at 80 years old.

Planning may ultimately tell you if $100,000 is enough but the process should help you also see the kind of stuff you are provisioning for.

You Can Try to Model the Frequency and Magnitude But Life May throw You a Weirder Curveball.

You can duplicate a few sheets and try to see different kind of pathways.

I feel that there would be some situations the sinking fund is inadequate. It cannot take care of all situations but if you are conservative, you have every right to set aside more.

This spreadsheet can help also figure out just how dramatic of crisis can your sinking fund address.

Having Runways Where You don’t Plan to Activate Your Sinking Fund That Much Can Alter How much You Need.

What does this mean?

If you buy a lot of investment style insurance policy for income you realize their income only starts maybe 5 or 10 years into the product and not immediately.

Which is another weird thing for me, and should raise your eyebrows what were they buffering for (hint: likely to let the advisers and insurance company earn and stabilize the commissions before extracting cash flow)

If you have a runway before the sinking fund is needed, and there won’t be any planned extraction, you might need a lower capital today. The spreadsheet can still work.

You could pair it up with insurance.

For example maybe before Kyith is 55 years old, when insurance is still relatively cheaper, be seriously well covered so that you need the sinking fund less

- Private shield

- Private rider

- Advanced stage critical illness

- Dunno whatever plan

This plan works because:

- You either have more capital buffer at 55 years old onwards, relative to your actual need.

- Longer time for the portfolio to have a chance to approach closer to median returns.

Needing the money immediately will pose a challenge, and a larger amount in the Sinking fund.

Revisiting My Critical Illness Sinking Fund

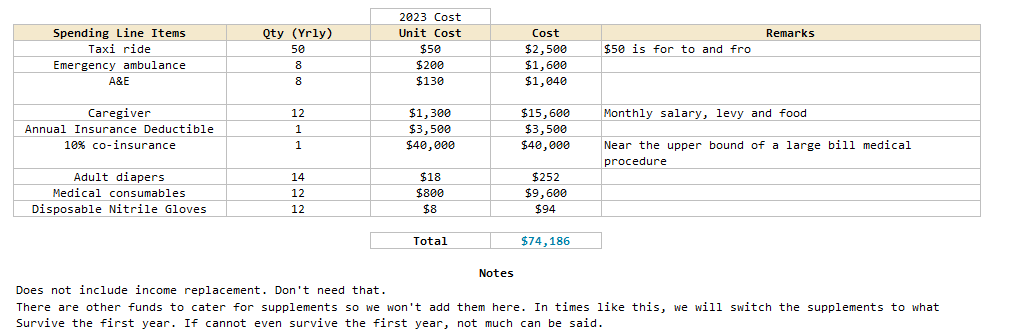

I want to see how this calculator did for my Critical Illness Sinking Fund article here. That was 3 years ago.

My Idea was to set aside $50,000 in 2023 in a 75% equity and 25% bond allocation. The actual need is 71 years old or later.

It is to budget for such a consideration:

The expense line items are in 2023’s cost. It works out to a total of $74,186.

We can see how the spreadsheet sees this:

Unfortunately, the plan to set aside $50,000 in 2023 would not do so well.

If the returns are good, no problem but I use a more pessimistic figure (rightly so for a more volatile portfolio), and if returns are challenging, even after 24 years, I might have to tap money from other areas.

The main difference between this plan and the other is the returns. The 7% and 3% p.a. vs a flat 4% p.a.

We cannot run away from how big of a determinant returns are. Even if you buy an endowment plan, or a higher return plan, you will still face this uncertain returns dynamics.

I hope this spreadsheet is helpful and feel free to play around, work out your sinking fund and let me know about it.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.