You may need to pay cash first for your bill before your health insurance plan will reimburse you the money if you decide to go through non-emergency (elective) treatments.

We have help enough of our clients file for their insurance claims after they were hospitalized at Havend. What I notice is that we have shield plan policyholders who were very surprised that they have to pay cash upfront for their medical treatment.

But aside from that, there are other situations where you might need to get ready cash upfront. Personally, I think aside from our need to build up an emergency fund, financial independence fund, funds for our kids’ education, we should try our best to build up a medical sinking fund that is specific for these medical needs.

I think many Singaporeans or those staying in Singapore might not be aware of the need to pay cash upfront or to put a deposit first so maybe I should spend some time to explain this.

What we are discussing today deals more with non-emergency (elective) treatments. These are the treatments where instead of going to the Accident & Emergency (A&E) department to get a problem checked out, you decide to look up a doctor at private or public hospital to treat a problem that has been bugging you.

Our Shield Plans are Based on a Reimbursement System

You pay for treatment first (or the hospital bills the insurer if there’s a direct billing arrangement).

Then, you submit a claim to your AIA, Prudential, Great Eastern, Singlife, HSBC, Raffles, Income insurer.

The insurer reviews the claim, and if approved, reimburses you or directly pays the hospital/doctor.

Typically, when you admit to the hospital, the hospital would require you to put a deposit. They will based the deposit based on the estimated size of your bill and also you as a patient.

There are two possible ways you can don’t pay the deposit or pay the deposit partially.

- Ask for a pre-authorization from your insurance company for this treatment you are about to undertake.

- A letter of guarantee (LOG) between your insurance company and the hospital to not have to pay the deposit or only pay partial deposit.

If you don’t have both, you might need to fork out cash upfront before the shield plan will reimburse you the money.

What is Pre-authorization?

Pre-authorization is like asking your insurance company for permission before you go for a big medical treatment — kind of like checking if your bill will be covered before you go ahead.

It’s your way of saying:

“Hey insurance, my doctor says I need this treatment — will you cover it?”

And the insurance company replies:

“Yes, we’ve reviewed it. It’s medically necessary and covered. Go ahead!”

Without pre-authorization: You might go for a surgery, pay the bill, then find out later your insurance won’t cover it or only pays part of it.

With pre-authorization:

- You get peace of mind before treatment starts.

- You avoid surprises — like rejected claims or uncovered items.

This may be a step by step example how pre-authorization works:

- Doctor says you need a surgery or hospital stay (non-emergency).

- You (or the clinic) submit documents to the insurer (diagnosis, cost estimate, doctor’s info).

- The insurer reviews your case and checks if:

- The treatment is medically necessary,

- It’s covered under your insurance policy,

- The doctor or hospital is on the insurer’s approved list (panel).

- If approved, the insurer gives you a Pre-authorization Certificate — basically a “green light” for the claim.

- You go for the treatment, and it’s much easier to claim afterward — sometimes the hospital can even claim directly.

Each of your insurer have made it simple for you to look up their panel of doctors, or extended panel of doctors so that you can submit your pre-authorization.

Do note: Out of all the insurer, Income Insurance is the only insurer that you CANNOT do pre-authorization. This means that Income policy holder would have to rely on LOG.

What is Letter of Guarantee (LOG)?

A Letter of Guarantee is like a note from your insurance company to the hospital that says:

“Hey, this person is covered by us. If the bill ends up high, we promise to pay part of it — up to this amount. So don’t make them pay the full deposit upfront.”

Without a LOG: Hospital says: “Your surgery might cost $20,000. Please pay a $20,000 deposit before we admit you.”

With a LOG:

- Insurance gives the hospital a guarantee letter (say, up to $10,000).

- Hospital says: “Okay, just pay the remaining $10,000.”

Sometimes if the LOG covers enough, you may not need to pay anything upfront (or just a small deposit).

Now… you need to understand that the LOG is not a blank cheque. It only covers up to a certain amount.

You’re still responsible for:

- Any amount above the LOG,

- Your deductibles and co-insurance, and

- Any treatment not covered by your policy.

I got from my colleague Jia Min Income Insurance, Singlife and HSBC Life’s Letter of Guarantee (LOG) Limits:

These are the three insurer that Havend carry currently.

What this means is that if your estimated bill size is greater than these limit, there is a chance that you got to put up some cash upfront. Technically, you may be able to use your CPF Medisave for some treatments but there are limits to it.

Notice the limits are higher for government restructured hospital but lower for private.

We all know that the bill size is much larger for private than public and your estimated bill can easily exceed $30,000 or $50,000 which means… you better have the cash flow upfront to pay for it.

I have checked the LOG limit for AIA, Great Eastern and Prudential and their limits is around this if not lower.

A Flow Chart to Summarize if You Might Need to Fork Out Cash Upfront for Your Medical Treatment

If you have obtain pre-authorization, then it is more straightforward but if you did not, it will depend on whether you have LOG and if you don’t, you are likely to pay a cash deposit.

However, if you have, whether you fork out cash will depend on your estimated bill size relative to the LOG Limit.

This is where you might need to pay cash.

All Pre and Post-Hospitalization Bills Have to be Fully Paid in Cash by the Policy Holder first.

Pre-hospitalization treatment are the medical care you received before you are admitted to the hospital and post-hospitalization are the care you received after you leave the hospital.

Example of a pre-hospitalization:

Let’s say you’re having stomach pain. You visit a doctor, get tests done (like blood tests or scans), and take some medications before the doctor decides you need to be hospitalized for surgery.

All those doctor visits, tests, and medicines before being admitted — that’s pre-hospitalization treatment.

Example of a post-hospitalization:

After surgery, once you’re discharged, you may need follow-up doctor visits, more tests, physical therapy, or medicines for a few weeks. All of this is part of post-hospitalization treatment.

These are based on reimbursement system.

This amount can come up to a few hundred or thousands of dollars.

How different is the reimbursement flow?

I think you get the idea.

Some Claims Process Might Take Longer than Usual

This implies that if you don’t set aside enough cash flow on hand, you might face some cash flow crunch.

This is not due to us not having adequate manpower but more on the insurer side.

Insurers can process claims pretty fast, like this table published by MOH. 75% of the claims can be done within 1-2 days.

In a nice flow:

- Hospital takes a few weeks (about 3) to file the claim.

- IP Insurer does it within 1-2 days.

- Hospital takes a few days or a week or so to reimburse you.

In a bad flow:

- The insurer will get further information from the doctor/hospital.

- A lot of back and forth multiple times before the claims is settled.

- We have seen such case drag out for as long as 6 months.

We seem to notice that there are more back and forth. When the medical bill size gets dearer and dearer, insurance companies are likely to do more due diligence.

I like to think there are more disputes by the insurer seeking more prove from Income Insurance because they are the only one who could not do pre-authorizations.

Singaporeans Need a Specific Medical Sinking Fund to Provide Liquidity for these Potential Out-of-Pocket Upfront Costs. And I Don’t Think We Should Consider the Money as Part of Our Emergency Fund.

All of this seemingly triangulate to potentially needing more upfront cash required if you need to do non-emergency medical treatment.

More and more, it points out that we might need to fund a medical sinking fund.

I don’t like to call it an emergency fund because emergencies are something that you don’t know what hit you. If I tell you that it is natural for humans to need a big fix once in a while upfront, would this be so much of a surprise? The surprise might be when the medical issue hit you but not so much if you have consider it.

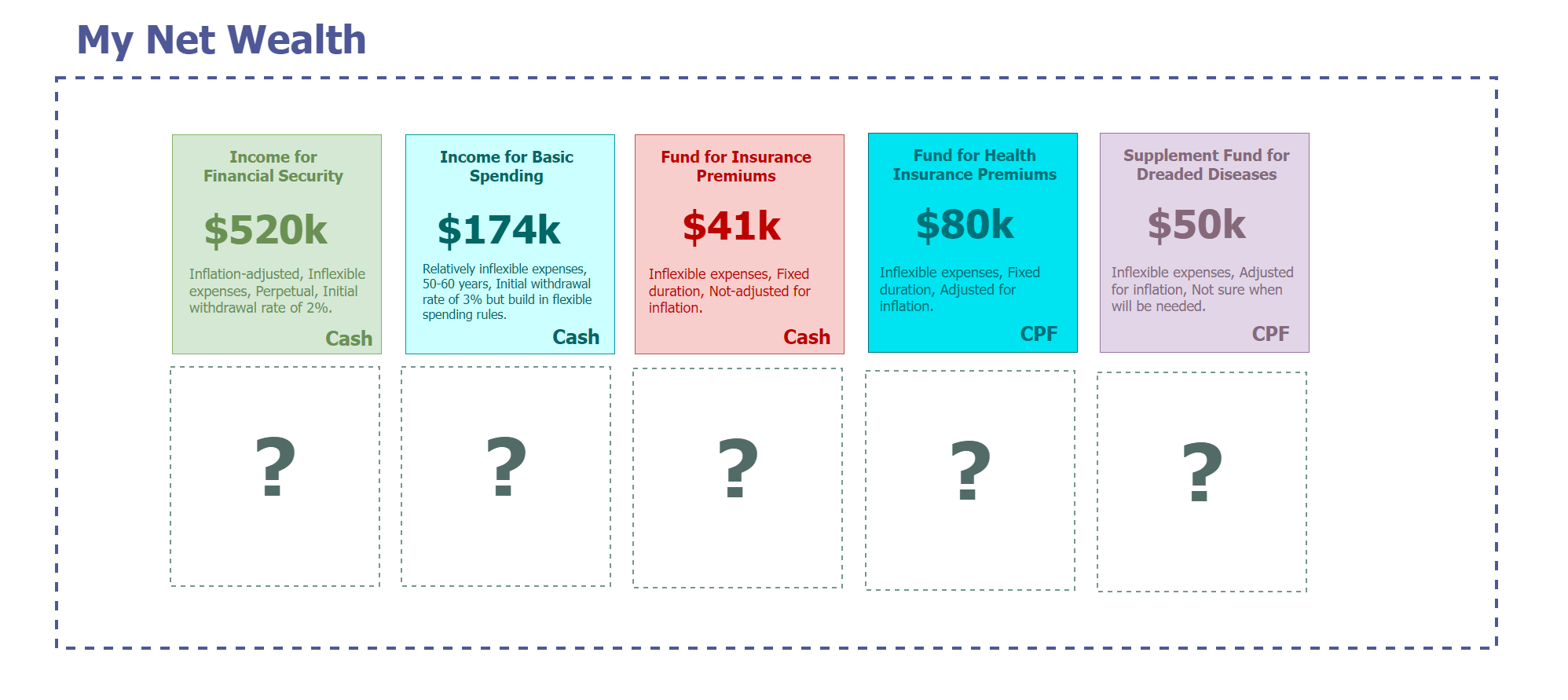

There are some of us who prefers to look at what we need when we are financially independent in one portfolio providing one income and there are some of us like myself who prefers to look at our plan more like separate portfolios of money with different allocations, that are oriented based on specific needs.

I prefer to do this because of a few reasons:

- In some of these money, we may need to ensure we spend from them consistently and with inflation-adjustment.

- Some, like our discretionary spending is consistent but up to a certain age, and we can be flexible.

- My insurance premiums paid by a “portfolio” in OA doesn’t go up with inflation.

- The need for upfront medical cost is needed but doesn’t take place all the time, so we just need to make sure that there is an adequate amount to supplement our needs.

The unique nature of the growth of the cash flow needs, degree of flexibility, how long the cash flow needs, the frequency of the need makes me think we should separate them out mentally or listed out so that we can examine them better.

But I won’t call the portfolios that I set aside a big pool of emergency savings. Think about this, as your emergency fund becomes bigger, have you thought of what kind and how many emergencies you need that fund to save? Is your fund big enough to save all of these emergencies?

The need for such a fund is greater if you have a preference for private hospitalization or wish to prepare for one.

These upfront cost can come up to a few hundred or thousands of dollars.

The idea is to try your best to build up because… if you are hit with something and you die die need to fork out cash, you will need to scavenge from your child’s education fund or your retirement fund. The money has to come from somewhere. Setting this aside is to allow you to size up how much money you have prepare for times like those and don’t have to scavenge from your other goals.

I always like the idea that even $20,000 set aside will make a lot of difference. “But Kyith, does $20,000 fortify you from all the potential upfront costs?” Well no, if your potential bill size is much larger (and we do see frequent bills larger than this!), but its better than not setting aside any right? You will also need to save up for your other goals right?

We need to balance between our commitment to our other financial goals and I think we should have an internal “ladder of priority” when it comes to how important each of them are. If you frequently have private treatments with non-panel doctors, then do prepare a bigger one!

I should also remind everyone that this is upfront which you may eventually get reimbursed. So this is a pool for liquidity rather than you are not gonna see the money again.

Why Some Singaporeans or Singapore Residents Can Be Shock That They Need to Pay Their Medical Cost First?

We do get a few of our clients who struggle to understand why they need to pay first.

Personally, I think that this is due to a few reasons:

- Many of us purchase these shield plans and their riders quite early in our lives,

- The advisers who explain these shield plans to us, operate in a medical and insurance climate that is unlike today,

- The pricing and structure of the different grades of medical treatment shield & rider plans, relative to the actual medical cost back then, created a feedback loop that eventually got pretty out of control,

- MOH, the insurers have subsequently come out with measures to address this out of controls by

- Forcing co-payment of insurance cost to the policyholders.

- Segmenting away very premium and expensive private treatments to non-panel treatments which may not be fully borne by the insure and have to be borne by policyholders.

- Making cancer drug and services cost non-as charged anymore,

- However, many of us live in our daily world where we are less acquainted with the evolution of our healthcare and insurance landscape and are therefore less aware of the changes,

- We may rely on the anecdotal sharing of our relatives, acquaintance and love ones in the past medical treatments, which may be carried during the time before all these changes (#4) came out,

- Sound personal finance mediums out there did not frequently mention that you need a medical sinking fund to prepare specifically for cash upfront costs. Thus, some may think it is more likely that we don’t have to pay cash upfront due to how the system work than we have to be pay due to how the system work.

I felt compelled to write this because I have a unique lens of partly working in the operations of insurance, and write about personal finance in my free time. While I don’t do any of the claims, operating close to the operations & servicing team and insurance specialist team allows me to adjust my lens just how prevalent this upfront costs can be.

The short summary is that shield and rider plans works on a reimbursement system and by right you have to pay upfront cash potentially. So make sure you prepare for some liquidity.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.