Oil above $100. The economy just lost 92,000 jobs. India opens

institutional silver buying in 19 days. And the mining industry

can’t respond.

On March 12, Brent crude closed above $100 per barrel for the first time since August 2022—after Iran’s new

Supreme Leader, Mojtaba Khamenei, declared that the Strait of Hormuz

must remain closed. The International Energy Agency responded by announcing the largest emergency reserve release in its

history: 400 million barrels, with the United States contributing

172 million from the Strategic Petroleum Reserve. The oil market

shrugged it off. Brent barely moved. Traders understood what the IEA

itself acknowledged in its March report: the war has created “the

largest supply disruption in the history of the global oil market,”

with Gulf countries cutting at least 10 million barrels per day of

production.

Meanwhile, silver is trading around $84 — essentially where it

was a week ago when I published Issue #9 of the Silver Catalyst newsletter. The consolidation has now extended into its

second week. Gold sits near $5,100. The gold-silver ratio holds at

60-62:1.

In Issue #7, I documented how the January-February crash revealed the widest

paper-physical divergence in decades. In the first free article from Issue #9, I covered the Iran war’s oil-silver transmission mechanism, the

COMEX delivery crisis (59% of registered inventory demanded in one

month), and AI’s $700 billion silver appetite. This article covers a

different set of forces—ones that are less dramatic than war

but potentially more consequential for silver’s structural

trajectory.

There are nine Deep Dives in this week’s premium Silver Catalyst issue, and in this free article, I’ll discuss three of them.

India’s SEBI Opens the Floodgates: A $970 Billion Allocation

Channel

On February 26, India’s Securities and Exchange Board (SEBI)

announced reforms permitting mutual funds to allocate up to 35% of

assets to non-core holdings, including gold and silver ETFs. A

separate SEBI circular on valuation methodology takes effect on

April 1 — now 19 days away — mandating that Indian ETFs

use domestic exchange-published spot prices rather than LBMA

international benchmarks. The practical consequence: Indian mutual

fund NAVs will reflect local demand conditions, where silver

typically trades at a premium to London.

India’s mutual fund industry manages approximately ₹81 trillion

(roughly $970 billion). Even modest allocation creates enormous

demand:

At 1% adoption, 34 Moz of new demand is roughly half the projected 2026 structural deficit. At 3%, the new demand exceeds the

entire annual deficit. At 5%, it represents roughly 20% of the total

global mine supply.

This isn’t speculative demand from retail traders. It’s

institutional capital with multi-year investment horizons, allocated

by fund managers operating within a regulated framework. Once funds

establish precious metals positions, they tend to maintain them

through market cycles.

India’s silver appetite was already extraordinary before the SEBI

reforms. The country imported roughly 180-190 Moz in

2025—approximately one-quarter of global mine supply. Silver

ETF inflows nearly tripled year-over-year to ₹234.7 billion. The

SEBI rule change adds an institutional channel on top of what was

already the world’s strongest physical silver market.

The April 1 effective date means this isn’t a distant possibility.

It’s a near-term catalyst with a specific activation date—19 days from today.

Stagflation, $100 Oil, and the Fed’s Impossible Position

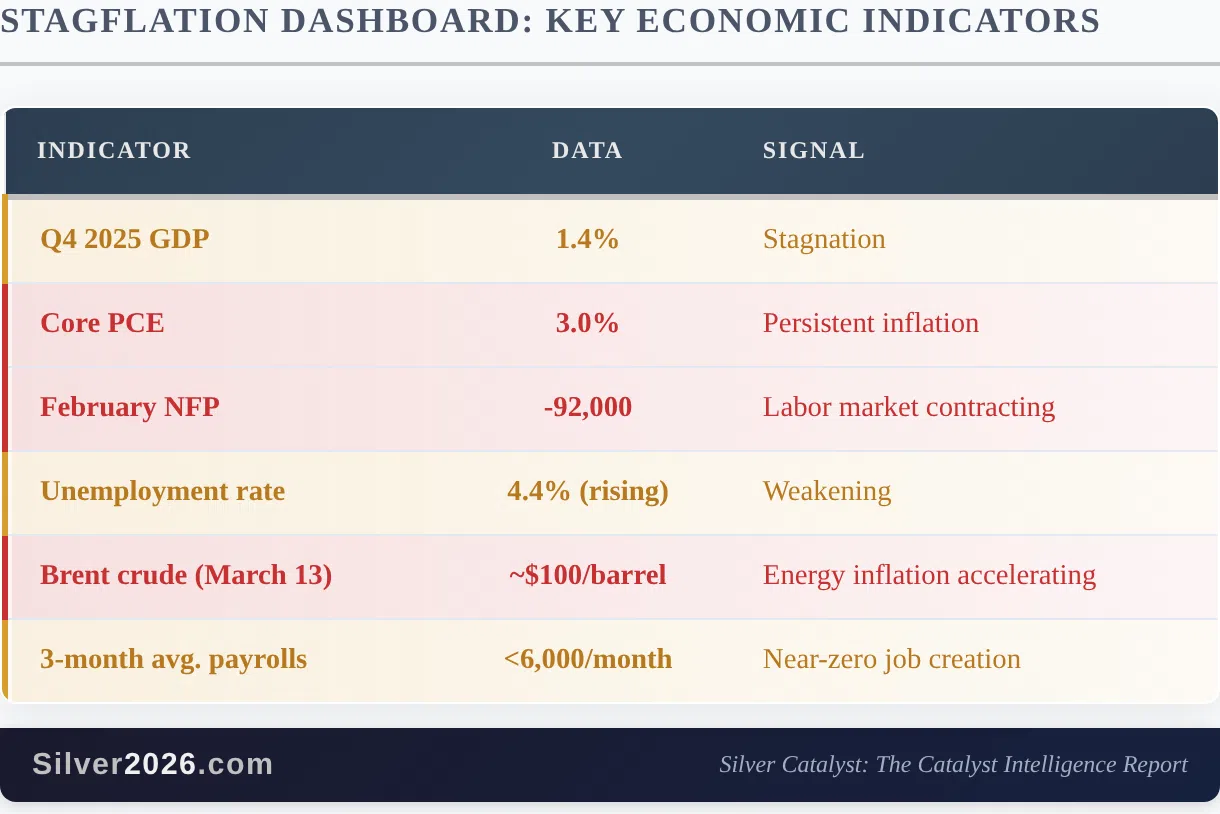

The February jobs report released on March 6 showed the US economy lost 92,000

jobs—dramatically worse than the consensus estimate of a

+50,000 gain. The unemployment rate rose to 4.4%. It was the third

time in five months that the economy lost jobs. The three-month

average now stands at fewer than 6,000 payrolls per month.

Separately, Q4 2025 GDP came in at just 1.4%. Core PCE inflation

remains at 3.0%. PPI rose 0.5% month-over-month.

Now layer oil above $100 on top of this.

This is the textbook definition of stagflation: economic growth

stalling while inflation persists and accelerates. The 1970s

demonstrated what happens to precious metals in this environment

— silver rose over 40% during the 1973-75 recession and from

$6 to $50 during the broader stagflation decade.

The Fed is paralyzed. Any rate increase to combat oil-driven

inflation would risk collapsing an economy already losing jobs. Any

rate cut would pour fuel on energy-driven inflation. The Warsh

nomination for Fed Chair remains unresolved; Powell’s term expires

in May, and FOMC minutes from February 18 revealed discussions of

rate increases — the first such discussion

in over two years.

Gold has responded by holding above $5,000, with central banks

buying an estimated 50-60 tonnes per month and China making 15+

consecutive monthly purchases. Silver benefits through ratio

compression — the gold-silver ratio has compressed from 100:1

to 60-62:1 over the past twelve months.

The Iran war didn’t create the stagflation setup. The macrodata was

already deteriorating before the first strike on February 28. What

the war did was inject a $100+ oil shock into an economy that was

already faltering — the classic mechanism through which

stagflation transitions from risk to reality.

The Broken Supply Response: Why $84 Silver Can’t Fix a Geological

Problem

Silver’s price has more than doubled from its 2024 levels. In a

functioning market, that kind of price signal should trigger a

supply response — new mines, expanded production, reactivated

projects. It hasn’t happened. And the data from the past two months

explains why it can’t.

Fresnillo PLC, the world’s largest primary silver producer, cut 2026

guidance to 42-46.5 Moz — down 9%. Hecla and First Majestic

are guiding lower. Mexico, which represents 25% of the global silver

supply, continues its moratorium on new mining concessions.

S&P Global’s mine cost outlook projected global weighted-average

silver AISC would rise 3.8% to $23.44/oz in 2026 — and that

was before oil crossed $100. With Brent now above

$100, energy costs have surged for every mining operation globally.

Every dollar increase in diesel raises extraction costs across the

70-80% of silver production that comes as a byproduct of base-metal

mining.

The structural constraints are binding:

The BHP-Wheaton $4.3 billion streaming deal, announced February 16,

is particularly telling. When the world’s largest diversified miner

locks up silver production at 20% of spot through the largest

streaming transaction in history, it signals institutional

conviction that physical silver is worth a historic premium to

secure. It also removes that production from the open market.

Mine development takes 15.7 years. Even if a mining company decided

today to develop a new primary silver deposit in response to $84

prices, the first ounce wouldn’t reach the market until 2042. The

supply cavalry isn’t coming.

What This Means

Three structural forces are tightening the noose around silver’s

supply-demand balance—and none of them can be resolved by

short-term price movements.

India’s SEBI reform opens an institutional channel into a nearly $1

trillion asset base in 19 days. The mining industry cannot respond

to price signals because of geological constraints, declining ore

grades, and a 15.7-year development timeline. And the macroeconomic

backdrop has shifted from “risk of stagflation” to “stagflation is

“here”—with oil above $100, the economy losing jobs, and the

Fed unable to act in either direction.

These aren’t speculative forces. India’s SEBI reform has a specific

date. The ore grade data are geological facts. The February jobs

report is published by the Bureau of Labour Statistics. The supply

deficit is in its sixth consecutive year. And the mining constraints

don’t ease because silver went from $30 to $84—they get worse

because the easy ore was extracted decades ago.

Silver’s current price of ~$84 reflects a market that has absorbed

the February correction and is consolidating. It does not yet

reflect the activation of a $970 billion institutional allocation

channel, the impact of $100+ oil on mining costs, or the full

stagflation transmission from energy prices to precious metals

demand. Those forces are incoming. The timeline is measured in days

and weeks, not months and years.

The structural supply-demand imbalance I just described is one

dimension of the 100-catalyst framework I analyze in “Silver Rising.” The full Issue #9 contains six more Deep Dives covering the

COMEX delivery crisis and the 59% inventory-to-demand ratio; the

Iran war’s direct oil-silver transmission channels; China’s export

controls creating a two-front supply squeeze; AI’s $700 billion

annual silver demand; market structure stress, including the CME

trading halt and Eric Sprott’s $300 projection; and solid-state

battery progress with the EU Digital Product Passport. If you want

to understand where this market is headed and stay informed as it

unfolds, I encourage you to get “Silver Rising” with complimentary 2-week access to the

Silver Catalyst newsletter.

Thank you.

Przemysław K. Radomski, CFA The Silver Engineer

Investorideas.com

is the go-to platform for big investing ideas. From breaking stock

news to top-rated investing podcasts, we cover it all.

Mining stocks -Learn more about our news, PR and social media,

podcast and content services at Investorideas.com