Since I started Financial Samurai in 2009, I have been on a mission to help readers achieve financial freedom sooner rather than later. And one of the core strategies I keep coming back to is encouraging readers to get neutral on real estate by first buying a primary residence. Once you have secured your primary residence, you no longer are at the mercy of ever rising rents. Inflation is too difficult a beast to defeat.

Once you get neutral real estate, you can eventually get long real estate by adding rental properties over time. Owning more than one property is the only way to really benefit from appreciation, unless you sell your primary for a profit and downgrade to a cheaper home.

But while I have been on this crusade since the housing market crashed in 2009, there has been an equally loud, if not louder, crusade against homeownership. I’m not sure why.

Perhaps it is the lingering psychological aftermath of the global financial crisis, where it is always easier to be against something after it has declined in value. Or perhaps it is because roughly 40% of Americans do not own homes, and most of them skew younger, with louder voices online.

I understand the skepticism. It is completely human to be against something you do not own. But when it comes to building wealth, the market does not care about your opinions. It cares about numbers. And for the average person, I genuinely believe it is easier to make more money on real estate than stocks.

Let me show you exactly what I mean comparing two exciting examples between real estate versus stocks.

Making Millions On A Home Is Easier Than You Think

I have a hobby that most people find a little strange: I go to Sunday open houses. Not because I am always looking to buy, but because it keeps me connected to the market, given ~40% of my net worth is in real estate.

I get a feel for pricing trends, pick up remodeling and interior design ideas, and get my steps in walking through neighborhoods I appreciate. It is one of the more enjoyable and educational ways I spend a Sunday afternoon.

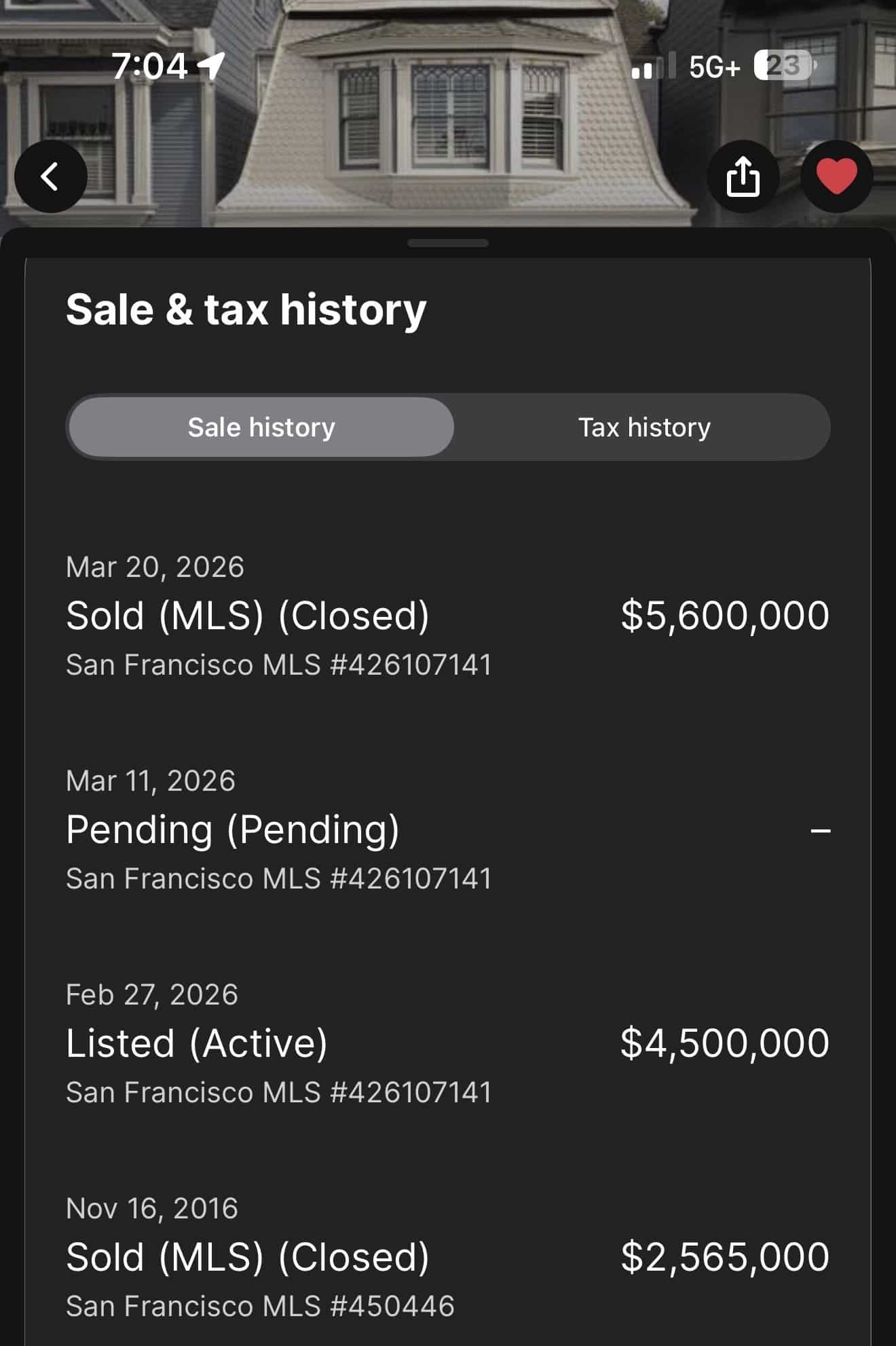

On one of those Sundays, I toured a single-family home in San Francisco listed at $4,500,000. It was a beautifully remodeled five-bedroom, questionable five-bathroom property with about 2,842 square feet – the kind of place my family would happily call home.

The downsides were it sat on a busy street between Cole Valley and Ashbury Heights, and the primary bedroom faced that traffic while offering only a three-quarter bath with a shower and two sinks, but no soaking tub or toilet. I’ve never seen that before, as the toilet was down the hall.

I made a mental note of it to check back in a month. Here’s the history.

Tremendous Price Appreciation

The buyer purchased the home in late 2016 for $2,565,000 with 20% down, putting $513,000 in as a down payment. Over the following years, I estimate they invested another $300,000 into a thoughtful remodel, opening up the downstairs layout, remodeling another bathroom, and adding a quarter bathroom upstairs. The work was done well.

Total cash invested: ~$813,000.

Ten years later, the home sells for $5,600,000. After real estate commissions, transfer taxes, and paying off the remaining mortgage balance, the seller walks away with approximately $3,600,000 in cash proceeds.

That is a 4.43 times multiple on invested capital and a 16% internal rate of return over ten years.

Let those numbers sink in for a moment.

The Numbers Get Even Better

Here is where homeownership starts to look genuinely extraordinary compared to almost any other investment.

If the sellers are married, they qualify for the federal capital gains exclusion on primary residences, which allows them to take up to $500,000 in profits completely tax free. That is not a loophole or a workaround. It is a benefit Congress deliberately built into the tax code to encourage homeownership, and it is one of the most powerful wealth building tools available to everyday Americans.

But the math gets even more interesting when you factor in the cost of living.

Over those ten years, the family had to live somewhere, which is why I say you’re only neutral real estate if you own a primary residence. If they had rented a comparable home in San Francisco instead, they would have spent somewhere between $2 million and $2.5 million in rent over that decade, money that would have disappeared entirely with nothing to show for it.

As a homeowner, the cost of the mortgage, property taxes, insurance, and maintenance was largely offset by what they would have paid in rent anyway. In other words, they essentially lived in a beautiful San Francisco home for free for ten years while their net worth quietly compounded in the background.

They raised their children there. They hosted dinners, celebrated birthdays, and built memories in a space that was entirely their own. And at the end of it, they walked away with $3,600,000.

How is that a bad investment? Please, feel free to tear up my argument if you’re against real estate.

The Confidence To Make A Large Investment

One of the most underappreciated aspects of real estate investing is the power of leverage. When you put 20% down on a home, you are controlling a $2,565,000 asset with just $513,000 of your own money.

In this example, the home appreciated by roughly $3,000,000 over ten years, before accounting for any remodel. That appreciation accrued entirely to the homeowner, not the bank. The mortgage lender got their interest payments. The homeowner got the wealth.

Try doing that with stocks. Under Reg T, the maximum margin allowed in a standard brokerage account is 50%, meaning you would need to put up $1,282,500 of your own money and borrow another $1,282,500 at steep margin rates, often 10% or higher for years. And that is assuming your brokerage will even extend you that much credit. More importantly, that borrowed money comes with no patience.

Margin calls in 2018, 2020, and 2022 forced countless investors to sell at exactly the wrong moment, locking in losses they never would have suffered if they had simply been able to hold. With real estate, the bank cannot call your mortgage because the market dropped 30%. With margin, your brokerage absolutely can, and will.

In practice, most people looking to deploy $2,565,000 into equities have the full amount in cash, precisely because of that volatility. The structural leverage advantage that real estate offers everyday investors simply does not exist in any other mainstream asset class.

Stocks Are More Volatile, Therefore Harder To Go All-In

This is why I have long argued that real estate is less risky than stocks, even with leverage. It is far easier to commit to a large down payment and leverage it 4x when you are buying something with tangible utility. Worst case, the home’s value drops, but you still have shelter for yourself and your family.

Stocks offer no such consolation. When they tank, you are left staring at red numbers on a screen, wondering why you didn’t take profits sooner. This is why few households that decide to buy a house and raise children will have a 100% equity position. A more appropriate 80/20, 70/30, or 60/40 equity/fixed income split would be more likely.

The Forced Savings Element

You have probably heard some version of this argument: renting is smarter than buying because you can invest the difference and come out ahead. On a spreadsheet, under ideal conditions, with perfect discipline, this can sometimes be true. The math is not wrong.

The human beings running that math, however, almost always are.

In theory, someone who rents and diligently invests the difference between their rent and a hypothetical mortgage payment for 30 years will accumulate significant wealth. In practice, the money gets spent. Lifestyle upgrades, vacations, a nicer car, private school.

The discipline required to execute that strategy perfectly for decades is extraordinarily rare. I have been writing about personal finance for 17 years, and homeowners in my readership consistently come out far ahead of renters who planned to save and invest the difference.

Homeowners, meanwhile, build wealth almost by accident. Every mortgage payment is a forced savings contribution. You do not decide whether to make it. Make it, or you lose the house. That behavioral constraint, which feels like a burden in the early years, turns out to be one of the most powerful wealth-building mechanisms available to ordinary people.

Not Everyone Can Buy In San Francisco. And That Is Okay.

The example above involves a $2,565,000 home with a $513,000 down payment and $300,000 in renovations. I am fully aware most Americans cannot replicate those numbers. That is not the point.

The point is the structure: leverage, forced savings, tax advantages, and utility all working together over time. That structure works in Columbus just as well as it works in San Francisco. It works in Raleigh, Austin, Nashville, and Boise. The dollar amounts change. The mechanics do not.

That said, I will make one ambitious argument.

You live in America, a country people spend years trying to reach, and you have the freedom to live and work anywhere within it. That freedom is worth using strategically. If you want to maximize your earning potential and your real estate appreciation, where companies are being built, where venture money is being deployed, where jobs are being created.

If your career and net worth are not growing the way you hoped, the answer might simply be geography. America gives you the freedom to change that.

But They Could Have Made More Investing In VCX!

Since I cherry-picked a top tier single family home sale in San Francisco, it is only fair to highlight a top tier equity investment with deep San Francisco roots: VCX, whose top three holdings are Anthropic, OpenAI, and Databricks, all headquartered in the city.

On paper, if that same $813,000 had been invested in VCX before its NYSE listing on March 19, 2026, the returns would have dwarfed the already impressive 4.4X real estate multiple by at least 2.5X at the moment.

But here is the thing. Nobody would have had the courage to put $813,000 into VCX right before the listing. Even fewer people had heard of Fundrise’s venture fund at all. And fewer still would have the discipline to hold on rather than sell after a double, triple, let alone a quadruple.

Buying A Single Family Home After Having A Baby Is Normal

Think about who actually buys a $2,565,000 home in San Francisco (about 37% above the median price back in 2016, and ~20% above today. They are a couple that likely earn between $400,000 to $700,000 a year, have significant living expenses, a net worth of around $1 – $3 million, and perhaps $300,000 left to find a remodel.

Earning $400,000 – $700,000 might sound like a lot, and it is. However, 23-year-old college graduates working in big tech earn $200,000 a year. If they marry another big tech colleague 10 years later, they are likely earning far more. And we have tens of thousands of these jobs here in the SF Bay Area.

To want to buy a single family home after getting married and wanting to start a family is absolutely normal. A majority of couples have this plan. Heck, I sold my old home, which turned into a rental for three years, for a similar amount back in 2017 to a couple with a one-year old. I wanted to simplify life because managing the property was a PITA and we had just had our first child.

Meanwhile, paying a 37% higher than median price for a single family home back in 2016 is still in the frenzy zone, where demand is elevated because so many people can afford up to the median price plus 50%.

Going All-In On A Venture Fund Is Abnormal

Conversely, investing the entire $513,000 down payment into a venture capital product you read about on Financial Samurai would be completely abnormal. Let me show you why.

First, you would have to have found Financial Samurai and kept reading until you read one of my articles about Fundrise’s venture product between 2022 and February 2026. Generously, that is a 10% chance. Most people find Financial Samurai through a search, read the article, and never subscribe to my newsletter or return on their own.

Then you would have to have had the conviction to invest in VCX before the listing based on my rationale. Given that the vast majority of people read but never act, call that a 5% chance.

Finally, you would have had to have invested a significant enough amount to generate $1 million or more in returns, as the homeowners did with their real estate. Even at a 10x return, that means putting in $100,000 to get $1 million, and $300,000 to match the homeowner’s return of $3 million. Fewer than 1% of readers had that conviction.

The math does not lie: 10% x 5% x 1% = 0.005%. One in 20,000.

A More Realistic Amount You Would Have Invested In VCX

The standard recommended allocation to alternative investments like venture capital is no more than 20% of a portfolio. So in practice, a couple in this position might have had the conviction to put $50,000 into the Fundrise’s venture product before its NYSE listing, but highly unlikely.

More realistically, they would have prioritized buying a home and living comfortably, putting perhaps $100,000 into the S&P 500, and maybe $10,000 – $20,000 into the venture product instead. Remember, they need to set aside $300,000 for remodeling. They either have most of it, or are saving their cash flow until they get it.

I say this as someone who has followed Fundrise’s venture product since the beginning in 2022. And even after thinking carefully about what the NYSE listing could mean for investors, I could only bring myself to invest $12,000 beyond my existing $1,000-a-month auto-invest for the past two years and my previous lump sum purchases.

With bombs flying, oil prices and interest rates rocketing, and the S&P 500 melting down, my conviction was lukewarm. In retrospect, obviously I should have invested a whole lot more.

No couple takes their entire home down payment and redirects it into a single alternative investment instead of buying a home to raise their family in. That is not how human beings actually make financial decisions.

The Wealth Building Stack

Here is how I think about building wealth, in the right order for most people.

First, buy your primary residence as soon as you can reasonably afford to. Negotiate hard, write the real estate love letter, use every edge available as I’ve shared in my archives. Every year you delay is a year of compounding you never get back.

Second, once your home is secured and your financial foundation is stable, aggressively rebuild your taxable brokerage portfolio. Continue maxing out your 401(k) and IRA throughout.

Third, as your brokerage portfolio grows over the next two to five years, consider adding a rental property. The combination of rising rents and appreciating prices, while costs remain largely fixed, is one of the most powerful long term wealth building engines that exists.

Fourth, once you have the core foundation in place – primary residence, maxed retirement accounts, a healthy taxable portfolio, and at least one rental – you can begin diversifying into passive real estate funds like Fundrise. This gives you exposure to markets beyond your backyard without the headaches of direct property management.

Fifth, if your foundation is strong and you have capital you can afford to be patient with, consider an allocation to venture capital funds. Private companies are staying private longer, therefore, it’s only logical to allocate more capital to private markets. Only if you are extremely wealth (net worth equal to 50X income or more) should you consider angel investing in individual companies. Most will lose all your money.

This is not a get rich quick stack. It is a get wealthy inevitably stack, built on boring, proven mechanisms that work for ordinary people in the real world. Skipping the first four steps to go all in on venture capital is highly risky. Build the foundation first.

The Bottom Line

The San Francisco home in our example was not purchased by an investing genius or a lucky speculator. It was purchased by a family who made a straightforward decision to buy a home they wanted to live in, improve it thoughtfully, and hold it for a decade.

The result was $3,600,000 in cash proceeds, a decade of free housing, $500,000 in tax free profits, and a lifetime of memories built inside walls they owned.

The anti homeownership crowd is welcome to poke holes in this argument. I genuinely mean that. The comments section is open.

But the numbers are the numbers. And after 17 years of writing about wealth building, I have yet to find a more reliable, more accessible, or more behaviorally sustainable path to making millions for ordinary Americans than buying a home, living in it, and letting time do the work.

Have you made significant money on a home? Or do you believe renting and investing the difference is the smarter long term play? Why do you think there is a growing voice against homeownership? I would love to hear your experience in the comments below.

Keep In Touch And Lend Some Support

If my writing has helped you financially over the years, the best thing you can do is pick up a copy and leave a positive review on Amazon for my books, Millionaire Milestones and Buy This, Not That, and leave a podcast review on Apple or Spotify. Every review means a lot.

And if you want more real-time thoughts on markets, real estate, the economy, and investment opportunities throughout the week, join 60,000 other subscribers and sign up for my free weekly newsletter. I have published three times a week since July 2009, when I helped kickstart the modern-day FIRE movement. Everything I write is based on firsthand experience.